# load packages

library(tidyverse)

library(broom)

library(mosaic)

library(ISLR2)

library(patchwork)

library(knitr)

library(coursekata)

library(kableExtra)

library(scales)

# set default theme and larger font size for ggplot2

ggplot2::theme_set(ggplot2::theme_minimal(base_size = 16))

# Create new variable

Credit <- Credit |>

mutate(Has_Balance = factor(ifelse(Balance == 0, "No", "Yes")))Categorical Predictors

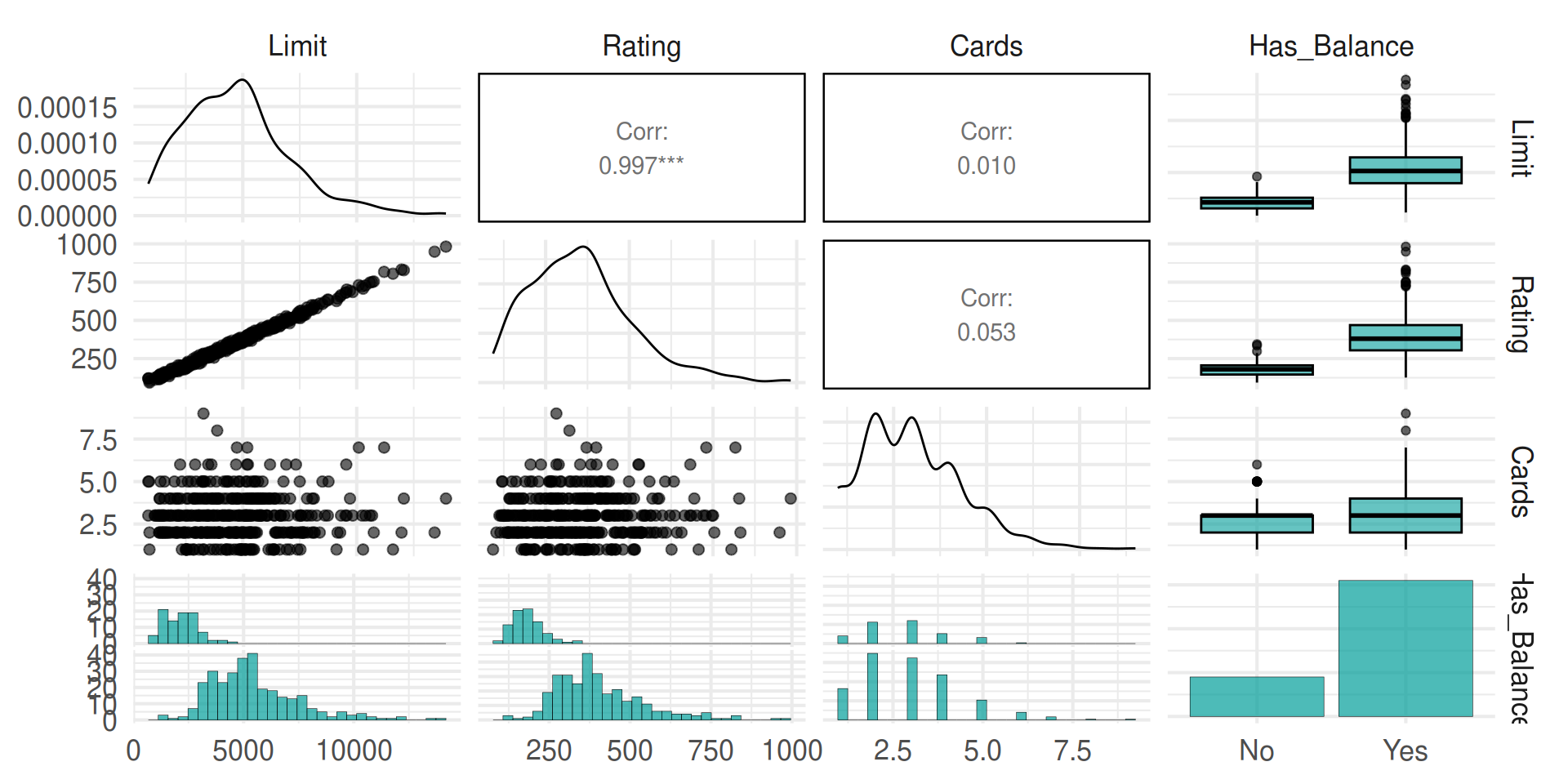

Outcome: Limit

| min | Q1 | median | Q3 | max | mean | sd | n | missing | |

|---|---|---|---|---|---|---|---|---|---|

| 855 | 3088 | 4622.5 | 5872.75 | 13913 | 4735.6 | 2308.199 | 400 | 0 |

Predictors

Code

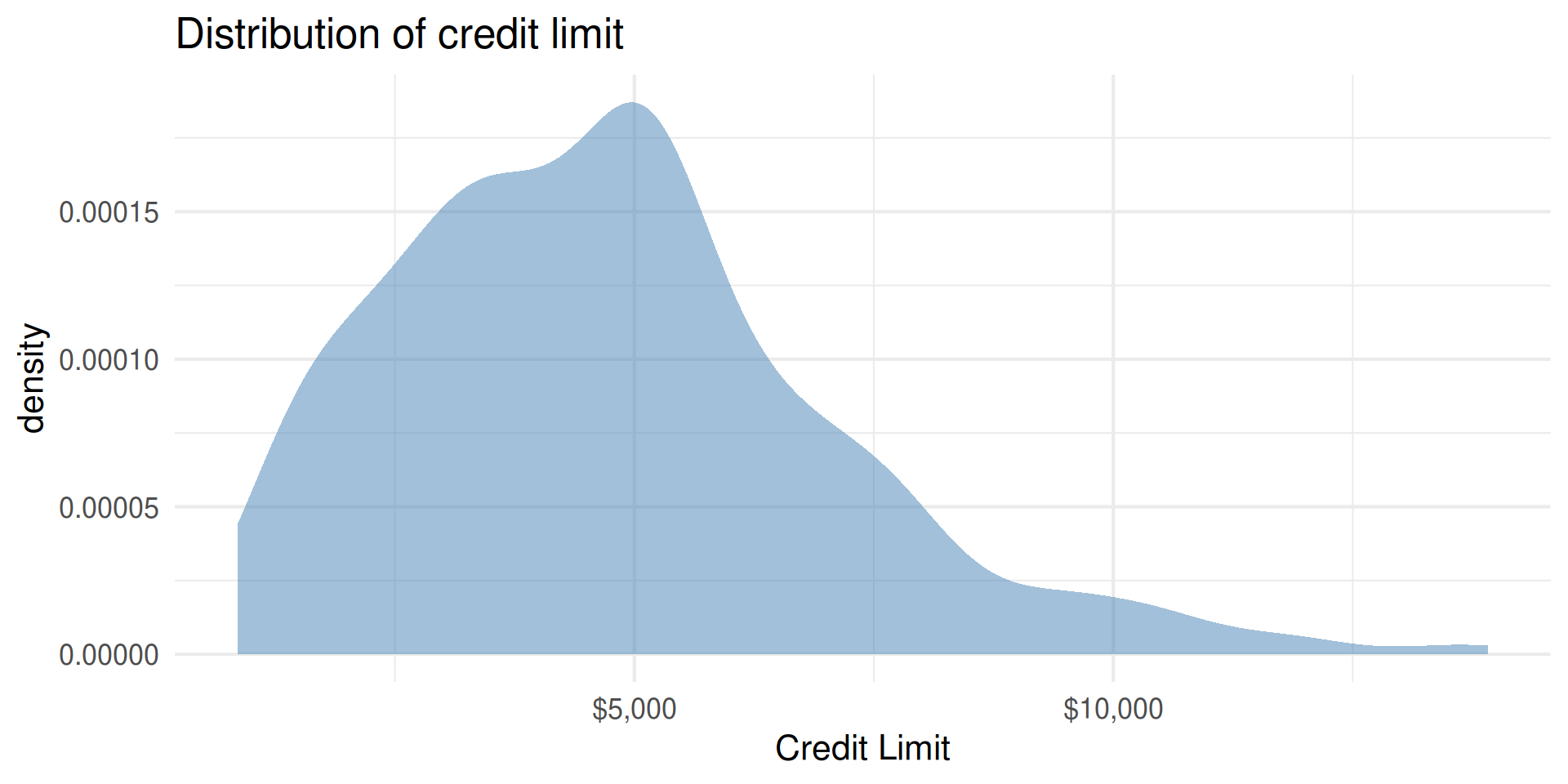

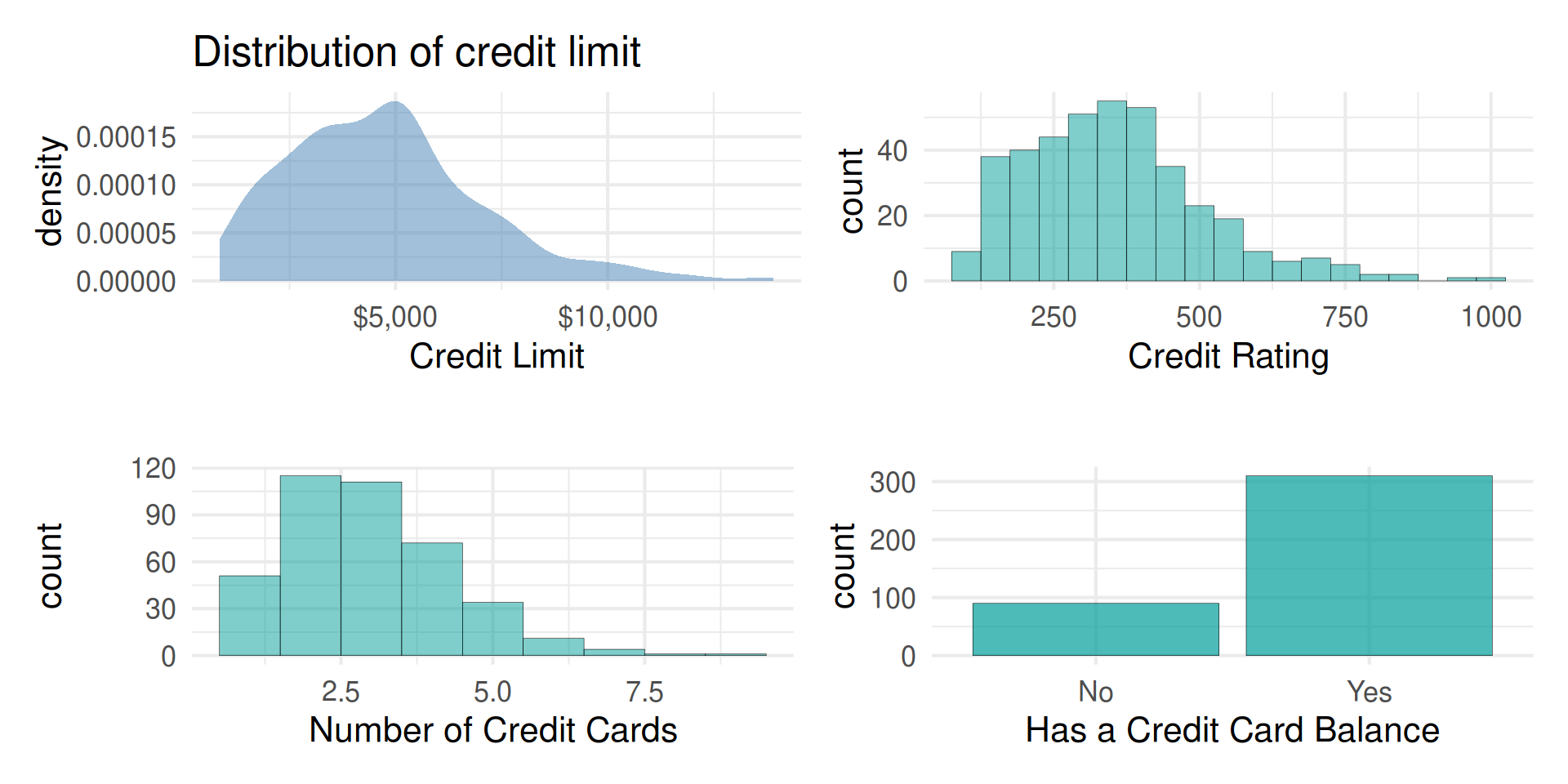

p1 <- Credit |>

gf_density(~Limit, fill = "steelblue") |>

gf_labs(title = "Distribution of credit limit",

x = "Credit Limit")|>

gf_refine(scale_x_continuous(labels = dollar_format()))

p2 <- Credit |>

gf_histogram(~Rating, binwidth = 50) |>

gf_labs(title = "",

x = "Credit Rating")

p3 <- Credit |>

gf_histogram(~Cards, binwidth = 1) |>

gf_labs(title = "",

x = "Number of Credit Cards")

p4 <- Credit |>

gf_bar(~Has_Balance)|>

gf_labs(title = "",

x = "Has a Credit Card Balance")

(p1 + p2) / (p3 + p4)

Outcome vs. predictors

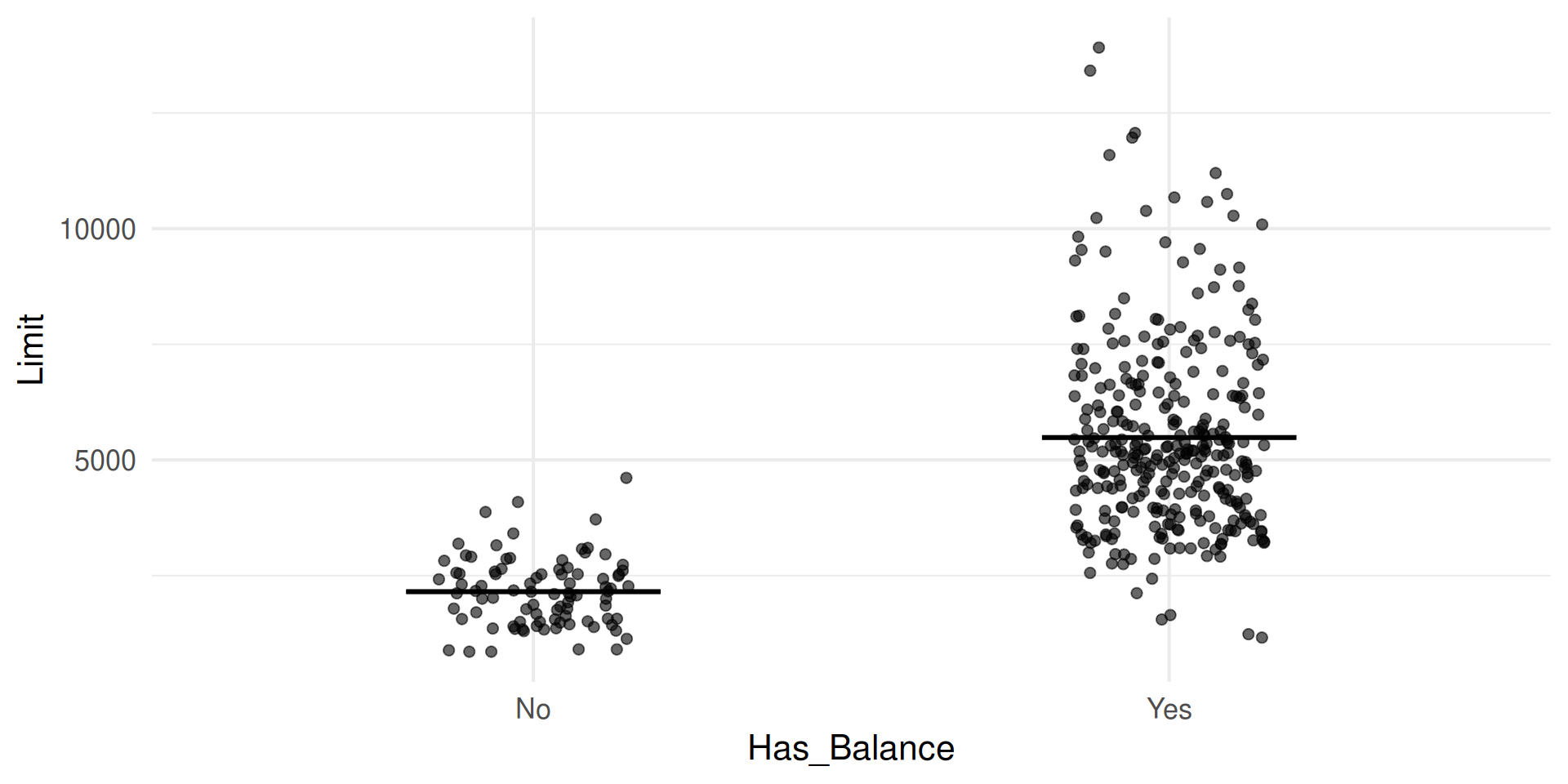

Interpreting Categorical Predictors

| term | estimate | std.error | statistic | p.value |

|---|---|---|---|---|

| (Intercept) | 2152.722 | 194.211 | 11.084 | 0 |

| Has_BalanceYes | 3332.746 | 220.609 | 15.107 | 0 |

- Where do we see each of the estimates in the plot?

- Where do we see the values we’d predict in the plot?

- (Trick Question) Are

Has_BalanceandLimitcorrelated? - On the board. Write down the dummy coding for an observation from each level in your chosen categorical variable.

Complete Exercises 2-4.

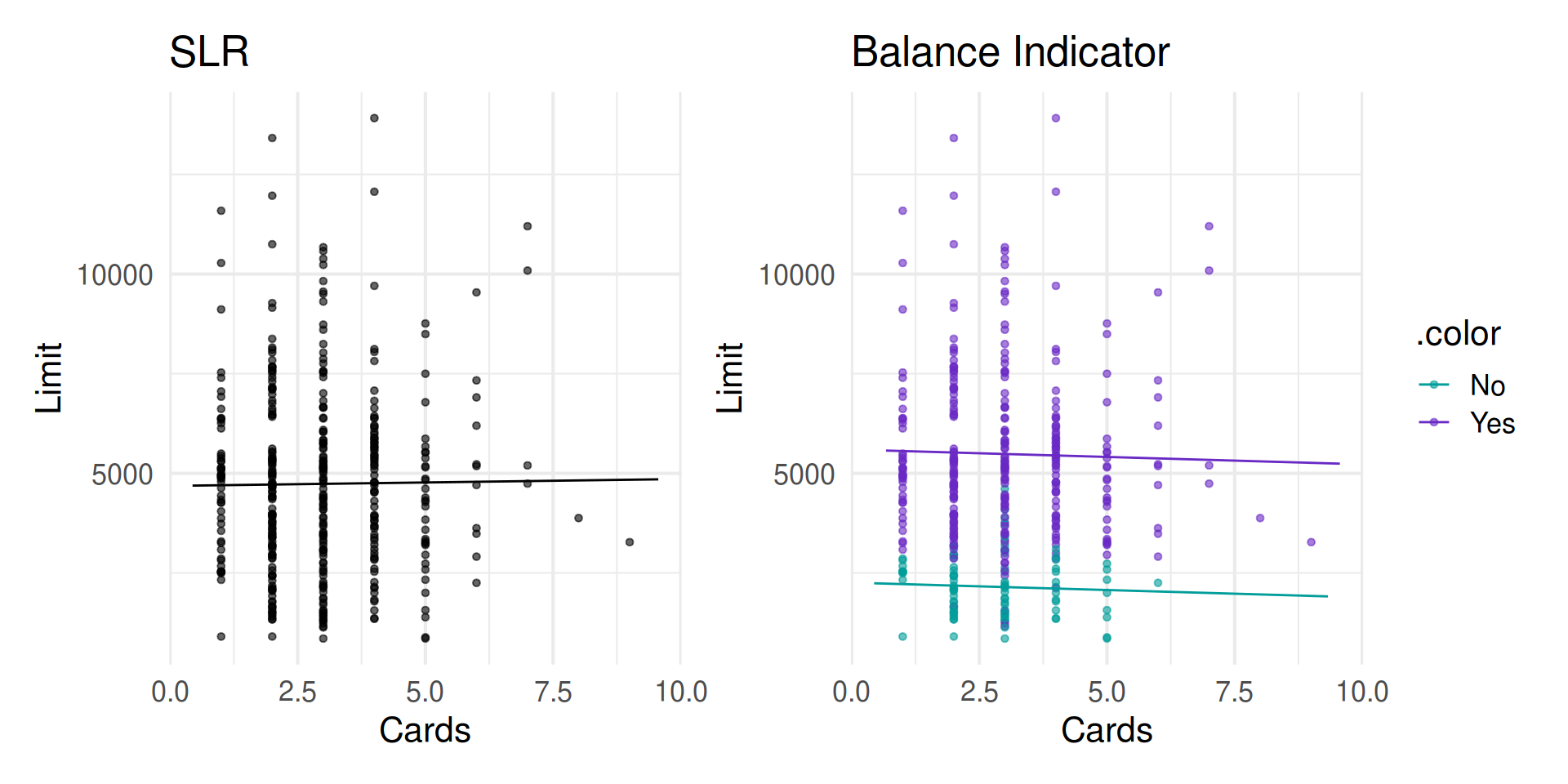

Credit Limit vs. Cards: parallel slopes

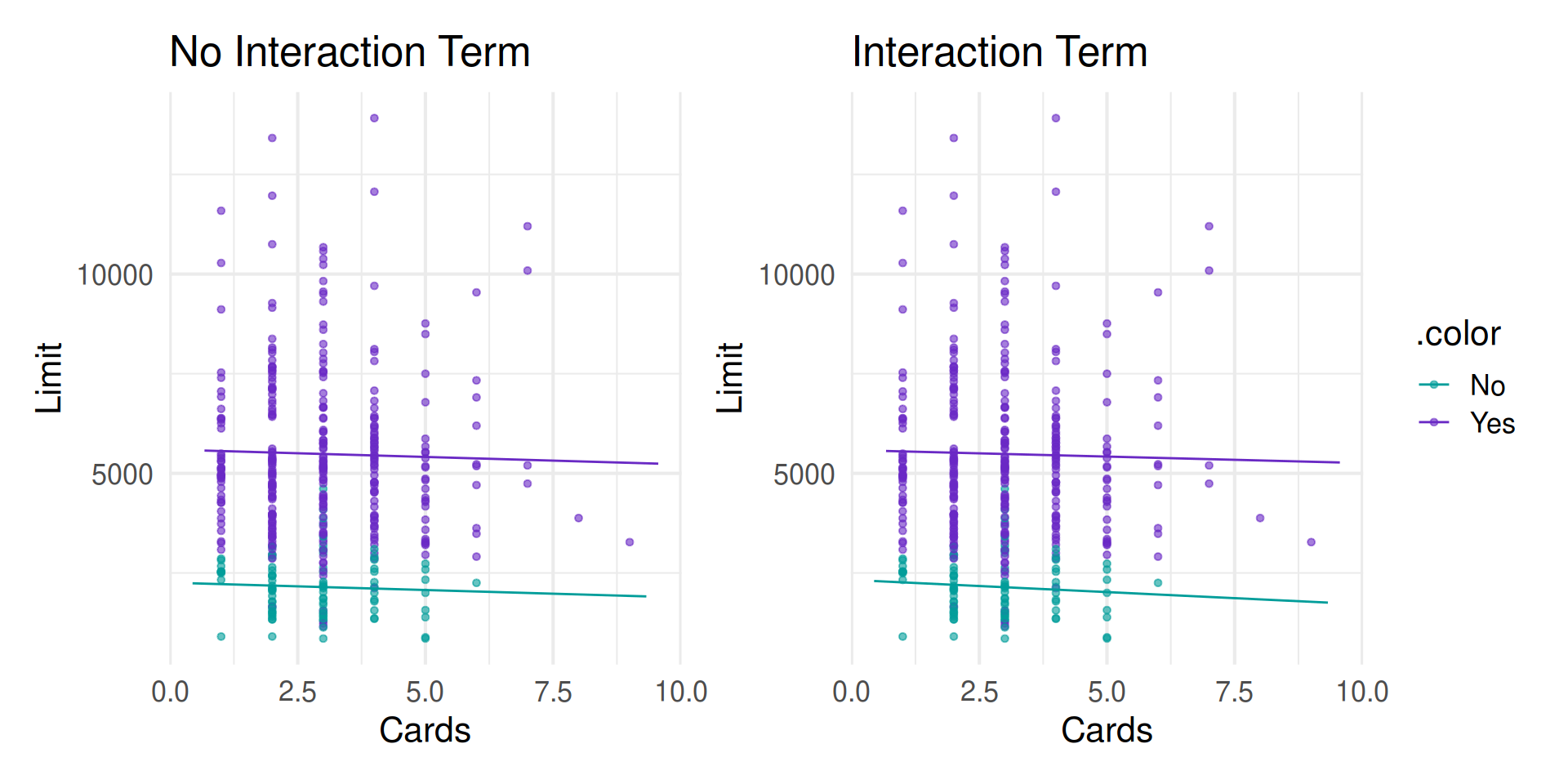

Interest rate vs. cards: interaction term

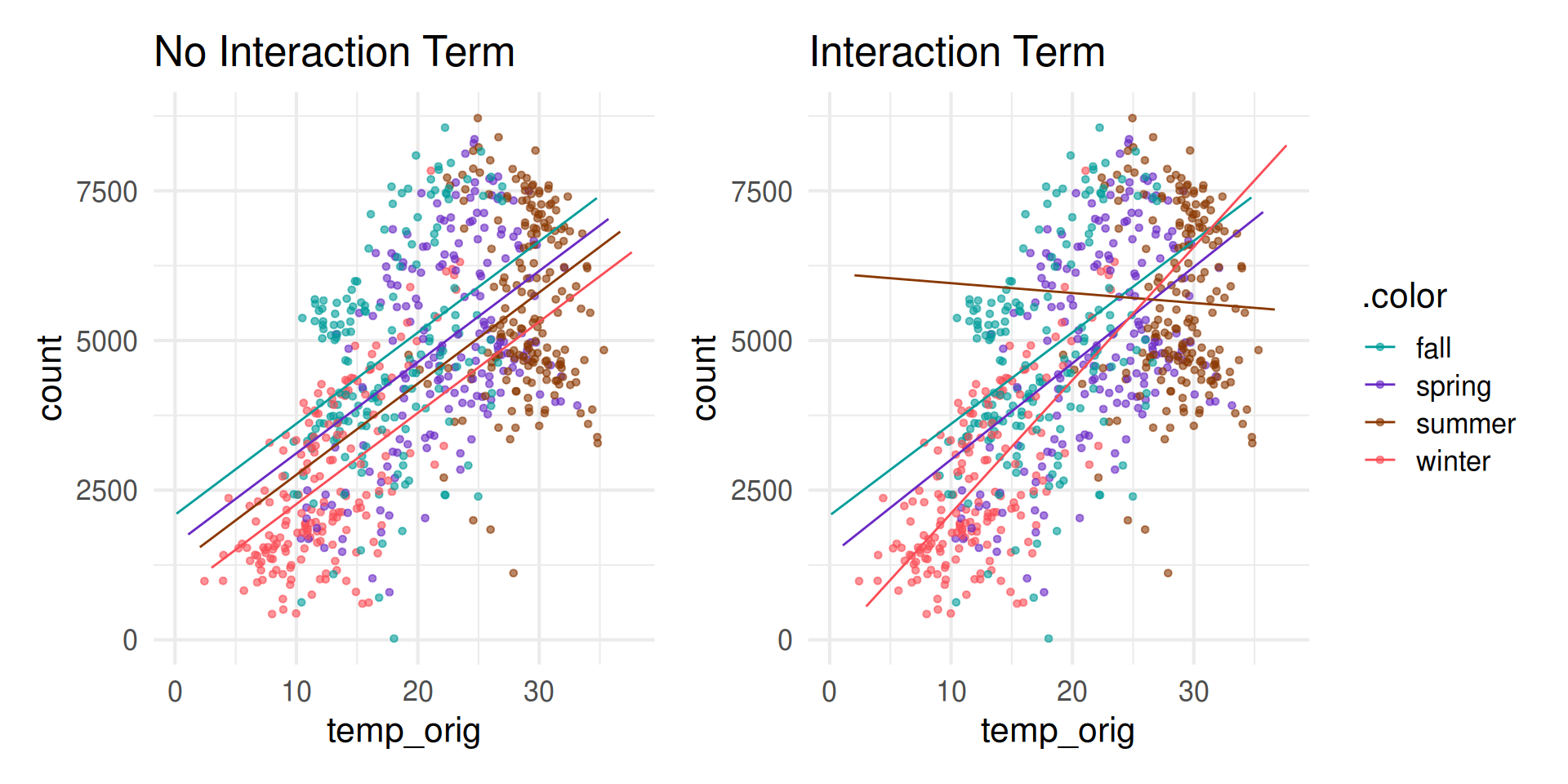

Bike Rentals vs. Temperature: interaction term